Register to get 3 free articles

Register to unlock the article and receive our free newsletter. Join 26,000 other hotel leaders and stay in the know.

Want unlimited access? View Plans

Already have an account? Sign in

Earlier this year, in its ‘As good as it gets? UK hotels forecast 2018’ report, PwC forecasted that 2018 would be a year of slower growth for the hotel industry. What impact could this have on existing hotels? SHEKINA TUAHENE investigates

[divider style=”solid” top=”20″ bottom=”20″]

The PwC cited a number of factors which may contribute to the predicted slow growth, including economic growth deceleration and the effect of the weaker pound on inbound tourism.

Another factor was the increase in room supply with the report stating that “a spike in new hotel supply, especially in London, will act as a drag” to the sector. According to data from AM:PM, a further 19,000 hotel rooms are scheduled to be added across the UK in 2018.

Metropolitan locations and popular regions which have already enjoyed increasing numbers in tourism are the areas of the country which will see the biggest influx of additional rooms. Of this total, over 7,000 rooms are expected to open in London. Other cities which have large pipelines for 2018 hotel room supply include Manchester, Belfast, Glasgow, Edinburgh, Liverpool and Bath.

Metropolitan locations and popular regions which have already enjoyed increasing numbers in tourism are the areas of the country which will see the biggest influx of additional rooms. Of this total, over 7,000 rooms are expected to open in London. Other cities which have large pipelines for 2018 hotel room supply include Manchester, Belfast, Glasgow, Edinburgh, Liverpool and Bath.

While the growth in the supply of rooms in the country must be coming as a result of the increased demand from guests and visitors, this may not be the best news for the hotel industry in the long run.

PwC’s UK hotels forecast for 2018 said, “We still forecast growth in 2018, but expect the inbound holiday boost from the weak pound to slow down. Inbound business travel trends are also reported down.”

In terms of statistics, this will affect occupancy levels as they will appear to decrease regardless of whether hotels sense the emptiness at ground level or not. For the UK hotel industry as a whole, an increase in rooms will mean that occupancy figures may not report as positively which could deliver a blow to the trade’s ego. Liz Hall, head of hospitality and leisure research at PwC explains, “Potentially it could impact trading and profits if demand weakens in areas that have seen large supply increases.”

The weakened pound brought about record-breaking levels of inbound tourism in 2017 outperforming 2016’s outstanding figures, implying that the increase in rooms may be the response that the country needs to be making. The UK set a record this year, when it welcomed 23.1 million visitors to its shores, figures from VisitBritain/VisitEngland’s 2016-17 annual review showed. Coupled with the increase in ‘staycations’, the number of people choosing to take a vacation in the UK may help to alleviate or balance out the number of hotel rooms being built.

The weakened pound brought about record-breaking levels of inbound tourism in 2017 outperforming 2016’s outstanding figures, implying that the increase in rooms may be the response that the country needs to be making. The UK set a record this year, when it welcomed 23.1 million visitors to its shores, figures from VisitBritain/VisitEngland’s 2016-17 annual review showed. Coupled with the increase in ‘staycations’, the number of people choosing to take a vacation in the UK may help to alleviate or balance out the number of hotel rooms being built.

However, occupancy levels have suffered as the past few years have not reported the best figures for the industry. This has been most evident in London and larger cities, due to terrorism threats and attacks which saw levels dip following most of the incidences.

An increase in supply could also have a negative impact on the price of hotel rooms as, if the demand isn’t there, hoteliers will find themselves having to reduce prices to attract guests, ultimately lowering profit margins. Hall confirms this, saying, “If occupancy struggles then it becomes harder to leverage room rates.” According to PwC’s report, of the 7000 rooms set to open in London, just under half of these rooms are “being developed in the budget sector.” Wooller has a relatively positive outlook on the growth of budget and midrange offerings in the sector saying that the “addition of rooms at varying price points” could be seen to help “the market attract a wider range of visitors on different travel budgets.”

This can also be largely affected by the types of rooms being offered and hotels being built, data published by HVS, AlixPartners AM:PM and STR, showed that budget hotel brands supplied 64% of rooms in the country in the first quarter of the year. Of the top 10 brands which had the largest supply as of 31 March 2017, eight were in the middle and budget range. Phillip Woller, area director, Middle East & Africa, STR said, “It’s interesting to note that the market is not just growing larger in size, but also in types of offerings available. Much of the new supply to come online over the past two years has been in the midscale segment, while historically, the upper tier hotel classes were the norm.”

If the average hotel room price is somewhere towards the lower end of the scale and visitors have a wider choice of such rooms, the increase in supply will inevitably drive down the price of hotel rooms in nearby properties in order to compete. Russell Kett, chairman of HVS, said: “The growth in budget hotels continues a trend in the hotel sector which is slowly but surely modernising the quality of affordable hotel stock, delivering greater consistency of product and great value for money.” He continued, “They are much cheaper to develop than full-service hotels, require less land, and can be developed on sites which are in secondary or tertiary locations, as opposed to prime city or town centre sites.”

It may also prove difficult for independent brands to compete not only with cheaper rooms but well known brands, as out of the 54% share that budget properties had, Premier Inn had the largest portion, “with more than 67,500 rooms in the budget segment, with growth running at 2.1%.” Travelodge was also a strong contender in the market with more than 39,500 rooms in the segment, closely followed by the budget brand of Holiday Inn owners IHG, HI Express, which had more than 16,200 rooms in the UK.

Considering the recognisability of such brands across the globe, independent hotels may possibly feel the effects of an increased room supply more than a larger hotel chain. This is more likely to happen in inner city and metropolitan areas, which tend to see higher numbers of visitors and may be dominated by large hotel chains. The report says, “The pipeline in regional room openings are also forecast to be above average with 2.4% [growth] in 2018 compared to an average between 2011 and 2016 of 1.1%.” It continued, “New supply is likely to continue to accelerate in selected cities outside London as developers take advantage of the buoyant market.” Again, affordable hotels from well known groups were attributed to much of the growth with the report saying, “The branded budget chains remain dynamic catalysts of this growth  accounting for over 40% of the UK active pipeline.”

accounting for over 40% of the UK active pipeline.”

Conversely, this is where boutique hotels and B&Bs may come into their own. BDO’s ‘Hotel Britain 2017’ report published earlier this year showed that the room yield for townhouse and boutique hotels increased by 7.9% to £255.03. A report conducted by estate agents Savills went on to show that the ‘experience trend’ was shaping the hotel industry, signifying a time for hotels in unique or remote settings to take advantage of the current fad. Hall echoes this sentiment, saying, “Clearly the sector needs new good quality accommodation supply; innovative concepts; environmentally advanced designs or it will stagnate.”

However, despite PwC’s predictions, the increase in new hotel builds does not necessarily mean that next year will be dire for the industry as Hall notes that the effects of a change in increase and demand may not always be evident immediately, if at all. She goes on say that building enough rooms for the increased demand is the process of “striking a balance” and if the record-breaking levels of inbound visitors continues or outperforms this particular elevation, it may not have as much of an impact as initially thought.

Hall says, “Although increases in demand for hotels stimulates the development of new hotels, the adjustment of supply to demand is not necessarily instantaneous or smooth.” She continues, “There tends to be a lag after the good times stimulate developers to pile in and then a dip in demand.”

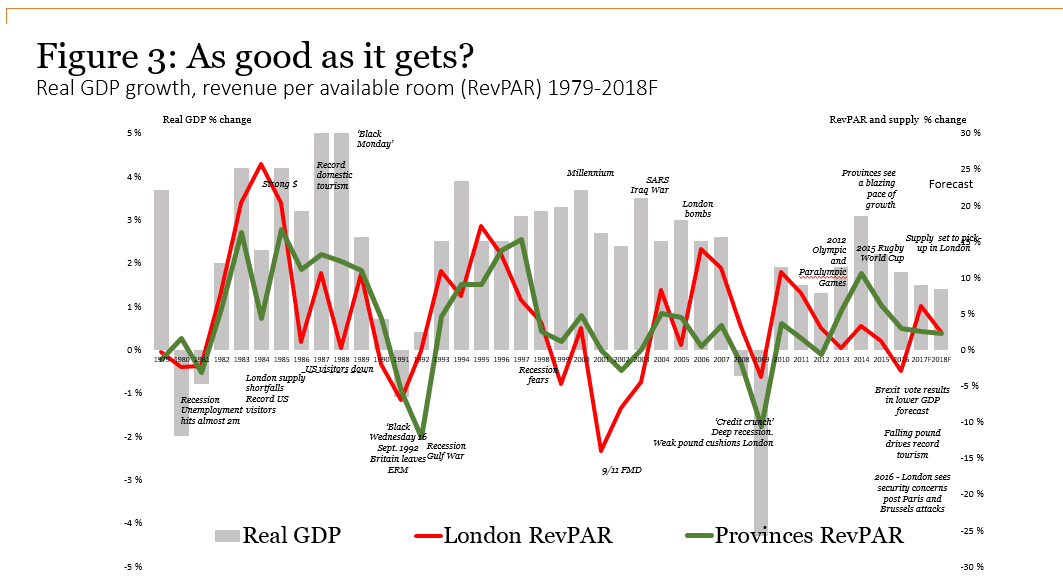

As with all trends, economies and longstanding industries, this is by all means, something that has been experienced in the UK sector before. Hall explains, “In the past we have seen periods when demand runs ahead of supply, creating shortages, high occupancy rates and high prices. This happened, for example in London between 1995 to 1997 – just one example – and the chart below shows all the things that boost and harm the sector.”

With 2018 getting nearer, only time will tell if the growth of the hotel industry will really show signs of slowing down over the next year. If so, the effects of that will have to be considered on a term-by-term basis, while heeding the predictions made by the PwC. Regardless of whether its impact is felt by the individual hotelier or not and whether that impact is felt immediately, the optimism felt by hoteliers according to a survey by Guestline proves that any outcome will be taken on the chin by the industry.